February 2011 Commentary

With the base rate at 0.5% since March 2009, we will soon be hitting two years of historically low interest rates. It seems clear then that the next move will be upwards, but it's far from clear when rates will start to rise. Driving the call for early rate increases is the currently high levels of inflation which are expected to persist throughout 2011. Mervyn King said last week that he expected inflation to peak at 4% or 5% and then drop back below 2% in 2012. This month's MPC minutes showed two members now voting for a rate rise, which shows increasing support within the MPC for early rate rises.

The opposing factor is the strength of the recovery and economic growth. The markets were surprised by the fall in Q4 2010 GDP announced last week. This points to a fragile recovery and the possibility of a double dip recession.

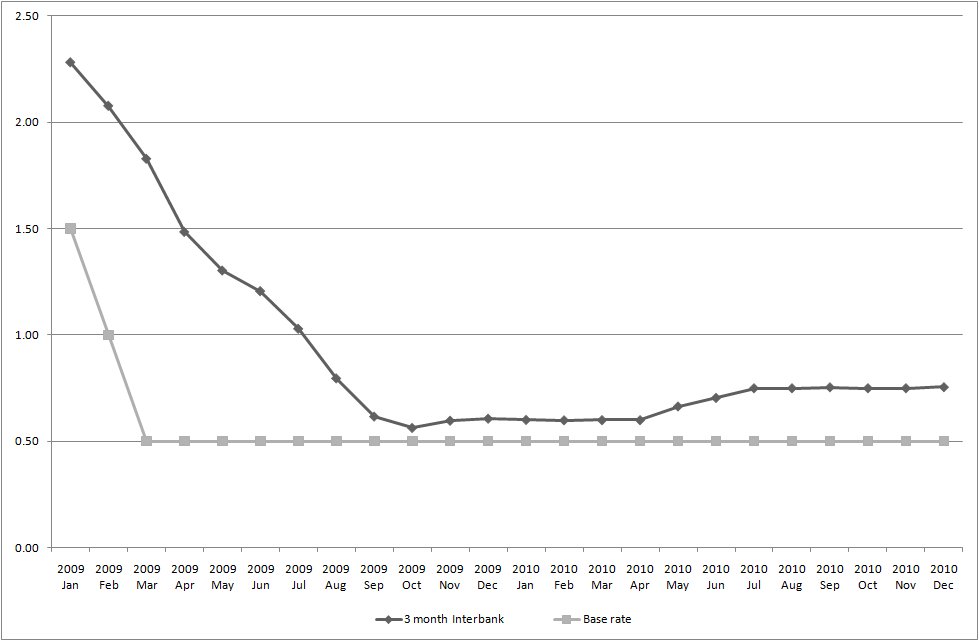

Looking at Interbank rates for the last two years, the graph shows that three month rates have nudged upwards during 2010, up 16bps from the start of the year.

Source: Bank of England Bankstats published 1st February 2011, Table G1.1

The NIESR Prospects for the UK Economy just published says that interest rates may well have to rise in the Spring to hold back inflationary pressures and that the case for further Quantitative Easing is evaporating. They are expecting the UK economy to grow by only 1.5% in 2011 and consumer price inflation to be 3.8% this year but fall back to 1.8% in 2012. The impacts of inflation mean that real disposable income will fall for the second successive year, by 0.8% in 2011.

So whilst rate rises seem a more likely prospect in 2012, the impact of increasing inflation will leave savers no better off.

|